All Categories

Featured

Table of Contents

Policies can likewise last up until defined ages, which in the majority of instances are 65. Past this surface-level details, having a better understanding of what these plans involve will certainly help ensure you acquire a policy that satisfies your needs.

Be conscious that the term you choose will certainly influence the costs you pay for the policy. A 10-year level term life insurance plan will certainly set you back less than a 30-year plan because there's less opportunity of an occurrence while the strategy is energetic. Lower threat for the insurance company corresponds to lower costs for the insurance holder.

Your family members's age ought to likewise influence your policy term option. If you have little ones, a longer term makes feeling due to the fact that it safeguards them for a longer time. If your children are near their adult years and will certainly be monetarily independent in the near future, a shorter term could be a better fit for you than a lengthy one.

Nonetheless, when comparing entire life insurance policy vs. term life insurance policy, it's worth keeping in mind that the latter typically sets you back less than the previous. The outcome is much more protection with lower costs, giving the ideal of both worlds if you require a significant quantity of insurance coverage yet can not manage an extra expensive policy.

What is Short Term Life Insurance? Explained in Simple Terms?

A degree death advantage for a term plan usually pays out as a swelling amount. Some degree term life insurance coverage companies permit fixed-period settlements.

Interest settlements got from life insurance policy policies are taken into consideration income and are subject to tax. When your level term life policy runs out, a couple of various points can occur. Some coverage terminates quickly without any option for revival. In various other circumstances, you can pay to extend the plan past its original date or convert it right into a long-term policy.

The downside is that your renewable level term life insurance policy will certainly come with greater premiums after its first expiry. Advertisements by Money. We might be made up if you click this advertisement. Ad For novices, life insurance coverage can be complicated and you'll have concerns you desire addressed prior to committing to any type of plan.

Life insurance firms have a formula for determining threat using death and rate of interest (What is a level term life insurance policy). Insurers have hundreds of clients obtaining term life plans at the same time and use the premiums from its energetic plans to pay enduring recipients of various other policies. These firms use mortality to estimate the number of people within a details team will certainly submit fatality claims annually, and that info is made use of to establish ordinary life spans for possible policyholders

Additionally, insurance provider can invest the cash they receive from costs and increase their revenue. Given that a level term policy does not have cash value, as a policyholder, you can't invest these funds and they do not offer retirement revenue for you as they can with whole life insurance policy policies. The insurance policy business can spend the money and gain returns.

The following area details the pros and cons of level term life insurance policy. Predictable costs and life insurance policy protection Streamlined plan framework Possible for conversion to permanent life insurance policy Limited protection period No cash money worth accumulation Life insurance coverage premiums can increase after the term You'll find clear advantages when comparing degree term life insurance to other insurance policy kinds.

How Does What Does Level Term Life Insurance Mean Protect Your Loved Ones?

From the moment you take out a policy, your premiums will never change, helping you prepare monetarily. Your coverage won't vary either, making these policies efficient for estate preparation.

If you go this course, your premiums will boost but it's constantly great to have some versatility if you desire to keep an energetic life insurance coverage plan. Renewable degree term life insurance is one more option worth considering. These policies permit you to keep your current plan after expiry, offering versatility in the future.

What is the Function of Decreasing Term Life Insurance?

Unlike a whole life insurance policy policy, level term coverage doesn't last forever. You'll pick an insurance coverage term with the ideal level term life insurance policy rates, however you'll no longer have protection once the plan expires. This disadvantage could leave you rushing to locate a new life insurance plan in your later years, or paying a costs to prolong your current one.

Several entire, global and variable life insurance policy plans have a money worth part. With one of those plans, the insurance firm deposits a part of your regular monthly premium payments into a cash money value account. This account earns rate of interest or is invested, helping it grow and supply a much more substantial payout for your recipients.

With a level term life insurance policy, this is not the situation as there is no cash value element. Consequently, your plan won't grow, and your survivor benefit will never ever raise, consequently restricting the payment your beneficiaries will certainly receive. If you want a policy that supplies a fatality benefit and builds money worth, check out whole, global or variable plans.

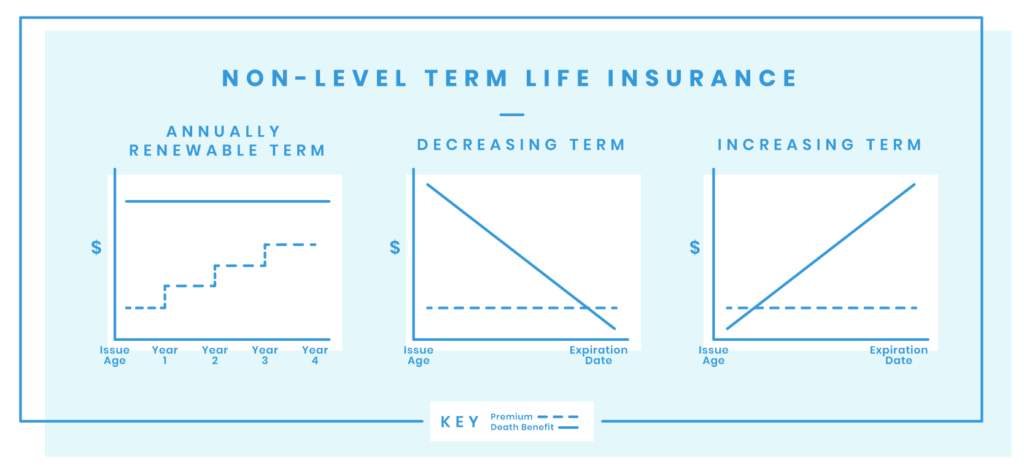

The second your policy runs out, you'll no more live insurance policy coverage. It's often feasible to renew your policy, however you'll likely see your costs boost considerably. This can offer concerns for retirees on a fixed revenue since it's an extra expenditure they might not be able to afford. Level term and reducing life insurance policy deal comparable plans, with the main difference being the death benefit.

It's a type of cover you have for a specific amount of time, referred to as term life insurance policy. If you were to die while you're covered for (the term), your liked ones obtain a fixed payout concurred when you take out the plan. You just pick the term and the cover amount which you could base, for example, on the price of increasing children until they leave home and you might use the payment towards: Assisting to pay off your mortgage, financial obligations, credit report cards or lendings Helping to spend for your funeral prices Aiding to pay university costs or wedding event expenses for your kids Assisting to pay living costs, replacing your revenue.

Why You Need to Understand Level Premium Term Life Insurance Policies

The policy has no money value so if your payments quit, so does your cover. If you take out a degree term life insurance plan you could: Pick a taken care of quantity of 250,000 over a 25-year term.

{kind=link}

Latest Posts

Cost Of Burial Insurance

Instant Term Life Insurance Quotes Online

Best Burial Insurance Policies